Is 62 your lucky number? If you're eligible, that's the earliest age you can start receiving Social Security retirement benefits. If you decide to start collecting benefits before your full retirement age, you'll have company. According to the Social Security Administration (SSA), approximately 69% of Americans elect to receive their Social Security benefits early. (Source: SSA Annual Statistical Supplement, 2019). Although collecting early retirement benefits makes sense for some people, there's a major drawback to consider: if you start collecting benefits early, your monthly retirement benefit will be permanently reduced. So before you put down the tools of your trade and pick up your first Social Security check, there are some factors you'll need to weigh before deciding whether to start collecting benefits early.

What will your retirement benefit be?

Your Social Security retirement benefit is based on the number of years you've been working and the amount you've earned. Your benefit is calculated using a formula that takes into account your 35 highest earnings years. If you earned little or nothing in several of those years (if you left the workforce to raise a family, for instance), it may be to your advantage to work as long as possible, because you'll have the opportunity to replace a year of lower earnings with a higher one, potentially resulting in a higher retirement benefit.

If you begin collecting retirement benefits at age 62, each monthly benefit check will be 25% to 30% less than it would be at full retirement age. The exact amount of the reduction will depend on the year you were born. (Conversely, you can get a higher payout by delaying retirement past your full retirement age--the government increases your payout every month that you delay retirement, up to age 70.)

However, even though your monthly benefit will be 25% to 30% less if you begin collecting retirement benefits at age 62, you might receive the same or more total lifetime Social Security benefits as you would have had you waited until full retirement age to start collecting benefits. That's because even though you'll receive less money per month, you might receive more benefit checks.

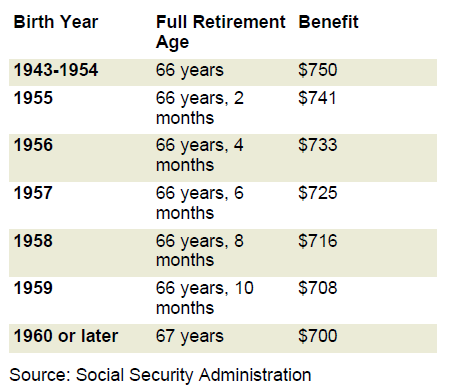

The following chart shows how much an estimated $1,000 monthly benefit at full retirement age would be worth if you started taking a reduced benefit at age 62.

If you want to estimate the amount of Social Security benefits you will be eligible to receive in the future under current law (based on your earnings record) you can use the SSA's Retirement Estimator. It's available at the SSA website at socialsecurity.gov. You can also sign up for a my Social Security account to view your online Social Security Statement at the SSA website. Your statement contains a detailed record of your earnings, as well as estimates of retirement, survivor's, and disability benefits, and other information about Social Security. If you're not registered for an online account and are not yet receiving benefits, you'll receive a statement in the mail every five years, from age 25 to age 60, and then annually thereafter.

Have you thought about your longevity?

Is it better to take reduced benefits at age 62 or full benefits later? The answer depends, in part, on how long you live. If you live longer than your "break-even age," the overall value of your retirement benefits taken at full retirement age will begin to outweigh the value of reduced benefits taken at age 62.

You'll generally reach your break-even age about 12 years from your full retirement age. For example, if your full retirement age is 66, you should reach your break-even age at 78. If you live past this age, you'll end up with higher total lifetime benefits by waiting until full retirement age to start collecting. However,unless you're able to invest your benefits rather than use them for living expenses, your break-even age is probably not the most important part of the equation. For many people, what really counts is how much >they'll receive each month, rather than how much they'll accumulate over many years.

Of course, no one can predict exactly how long they'll live. But by taking into account your current health,diet, exercise level, access to quality medical care, and family health history, you might be able to make a reasonable assumption.

How much income will you need?

Another important piece of the puzzle is to look at how much retirement income you'll need, based partly on an estimate of your retirement expenses. If there is a large gap between your projected expenses and your anticipated income, waiting a few years to retire and start collecting Social Security benefits may improve your financial outlook.

If you continue to work and wait until your full retirement age to start collecting benefits, your Social Security monthly benefit will be larger. What's more, the longer you stay in the workforce, the greater the amount of money you will earn and have available to put into your overall retirement savings. Another plus is that Social Security's annual cost-of-living increases are calculated using your initial year's benefits as a base--the higher the base, the greater your annual increase.

Will your spouse be affected?

When to begin receiving Social Security is more complicated when you're married. The age at which you begin receiving benefits may significantly affect the amount of lifetime income you and your spouse receive, as well as the benefit the surviving spouse will be entitled to, so you'll need to consider how your decision will affect your joint retirement plan.

Do you plan on working after age 62?

Another key factor in your decision is whether or not you plan to continue working after you start collecting Social Security benefits at age 62. That's because income you earn before full retirement age may reduce your Social Security retirement benefit. Specifically, if you are under full retirement age for the entire year, $1 in benefits will be withheld for every $2 you earn over the annual earnings limit ($19,560 in 2022).

Example: You start collecting Social Security benefits at age 62. You continue working, and your job pays $30,000 in 2022. Your annual benefit would be reduced by $5,220 ($30,000 minus $19,560, divided by 2).

Note: If your monthly benefit is reduced in the short term due to your earnings, you'll receive a higher monthly benefit later. That's because the SSA recalculates your benefit when you reach full retirement age, and omits the months in which your benefit was reduced.

Other Considerations

In addition to the factors discussed here, other financial considerations may influence whether you start collecting Social Security benefits at age 62. How do other sources of retirement income factor in? Have you considered how your income taxes will be affected? What about personal considerations? Do you plan on traveling, volunteering, going back to school, starting your own business, pursuing hobbies, or moving to a new location? Do you have grandchildren or elderly parents whom you want to help take care of? Every person's situation is different.

For More Information

Social Security rules can be complex. For more information about Social Security benefits, visit the SSA website at socialsecurity.gov, or call (800) 772-1213 to speak with a representative. You may also call or visit your local Social Security office.

We’re here to help! Contact Sentinel Benefits & Financial Group for the guidance you need.

This article is not intended to be exhaustive nor should any discussion be construed as legal or financial advice.